Introduction

Cosmetic surgery is often a significant personal and financial decision. The advertised procedure price may represent only one part of the amount a patient will eventually spend.

When treatment takes place outside the patient’s country, the budget may also include flights, accommodation, medical tests, medication, local transportation, insurance, follow-up appointments and extended stays during recovery.

Unexpected complications can increase these expenses considerably. The Centers for Disease Control and Prevention advises medical travellers to plan for possible additional care because complications after returning home may require prolonged treatment and may not be covered by regular health insurance.

Financing may make treatment appear immediately affordable, but every borrowing method creates different costs and responsibilities. Patients should therefore compare the complete repayment amount, not simply the monthly instalment.

BestCosmeticHospitals.com can help patients begin comparing cosmetic hospitals, surgeons, destinations, procedures and estimated costs. However, all quotations, financing agreements, insurance conditions and medical credentials should be verified independently.

Understanding the Complete Cost of Cosmetic Surgery

A reliable budget begins with the complete cost of treatment rather than the hospital’s starting price.

The total amount may contain four major categories:

- Medical treatment costs

- International travel expenses

- Recovery and aftercare expenses

- Financing and unexpected costs

A low procedure price can become much higher after these additional items are included.

Medical Treatment Costs

The medical portion may include:

- Surgeon’s fee

- Assistant surgeon’s fee

- Hospital or operating-room charges

- Anesthesia fee

- Preoperative consultation

- Blood tests

- Imaging and diagnostic tests

- Implants or medical materials

- Medication

- Compression garments

- Overnight hospital care

- Nursing services

- Routine follow-up appointments

Patients should request a written, itemized quotation rather than relying on a package headline.

International Travel Costs

Treatment outside the country may require spending on:

- Passport or visa

- Flights

- Baggage charges

- Airport transfers

- Local transportation

- Hotel or recovery accommodation

- Meals

- Companion travel

- Travel insurance

- Mobile communication

- Translation assistance

- Additional nights before and after surgery

Travelling during peak seasons or changing a return flight after surgery can increase the budget.

Recovery and Aftercare Costs

Aftercare may involve:

- Wound-care supplies

- Additional medication

- Drain or stitch removal

- Physiotherapy

- Follow-up imaging

- Local doctor appointments

- Nursing support

- Extra accommodation

- Changes to return flights

- Treatment of complications

- Revision consultations

Patients should ask who is financially responsible when recovery takes longer than expected.

Financing Costs

Borrowing can add:

- Interest

- Processing fees

- Annual fees

- Late-payment charges

- Currency-conversion costs

- International transaction charges

- Early repayment charges

- Insurance attached to a loan

The financing cost should be added to the treatment budget rather than treated as a separate issue.

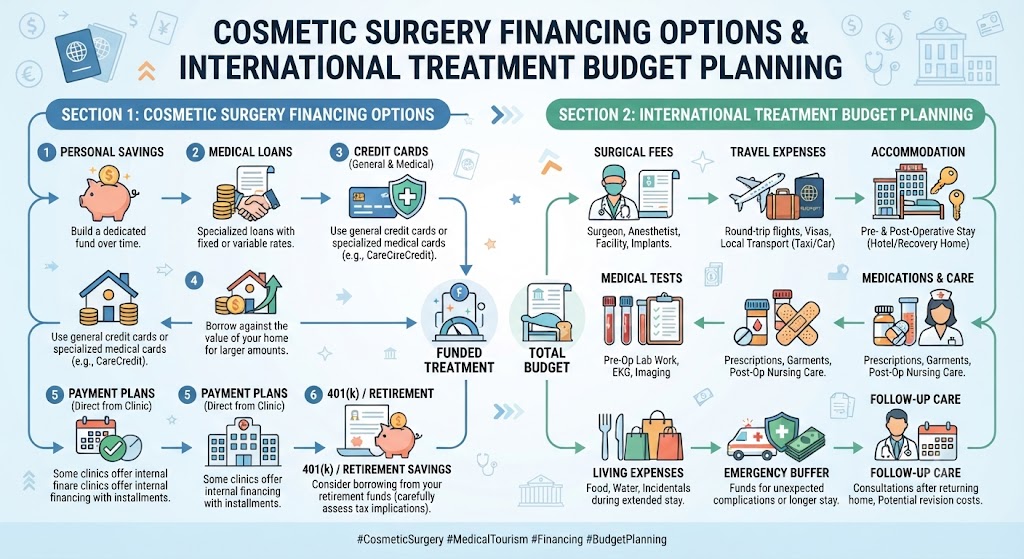

Cosmetic Surgery Financing Options

No financing method is automatically right for every patient. The suitable choice depends on income, savings, credit history, repayment capacity, procedure urgency and the terms available in the patient’s country.

Because most cosmetic procedures are elective, delaying treatment while saving may be financially safer than accepting expensive credit.

1. Personal Savings

Using savings avoids interest and loan repayments.

Patients can create a dedicated treatment fund and contribute to it regularly. This method provides time to research hospitals, compare surgeons and prepare for recovery without pressure from a lender or provider.

Savings should not leave the patient unable to pay for:

- Housing

- Food

- Existing loan repayments

- Family responsibilities

- Insurance

- Routine medical care

- General emergencies

The procedure should not use money reserved for essential living expenses.

Advantages

- No interest

- No credit check

- No monthly debt

- Greater control over the treatment date

- Easier cancellation when medical concerns arise

Limitations

- Treatment may need to be delayed

- Savings can take time to build

- Using all available savings may remove the emergency reserve

A separate savings fund for known future expenses is sometimes called a sinking fund. It can help patients build the required amount gradually instead of borrowing the entire cost.

2. Hospital or Clinic Payment Plans

Some cosmetic hospitals allow patients to pay in instalments before treatment. Others work with external financing companies.

Before accepting a provider payment plan, ask:

- Is the plan operated by the hospital or a lender?

- Is interest charged?

- What is the total repayment amount?

- When does repayment begin?

- Must the balance be cleared before surgery?

- Are administration fees included?

- What happens if surgery is cancelled?

- Is the deposit refundable?

- Can the treatment price change after financing approval?

- What happens if the surgeon or hospital changes?

A hospital payment plan may be useful when it is interest-free and transparent. However, it should not pressure the patient into proceeding with treatment before they are medically or financially ready.

3. Unsecured Personal Loans

A personal loan provides a lump sum that is repaid through scheduled instalments, usually with interest.

Personal loans commonly have fixed monthly payments over an agreed term, although actual structures vary by lender and country. Patients should compare the annual percentage rate, total repayment amount, fees and early-settlement rules rather than considering only the monthly payment.

Advantages

- Predictable instalments when the rate is fixed

- A defined repayment period

- May cover treatment and travel together

- May cost less than some medical credit products

Risks

- Interest increases the procedure’s total cost

- Missed payments can affect credit history

- Longer loan terms can make a procedure appear cheaper while increasing total interest

- Repayments continue even if the result is disappointing

- The loan remains payable if surgery is cancelled after non-refundable costs arise

Patients should avoid borrowing an amount that prevents them from meeting essential monthly expenses.

4. Medical Credit Cards and Healthcare Financing

Some countries offer credit products designed specifically for medical, dental or cosmetic treatment.

These may advertise:

- Zero-interest periods

- Deferred interest

- Low initial repayments

- Quick approval

- Treatment-specific credit limits

Patients must read the full agreement carefully.

The Consumer Financial Protection Bureau warns that some deferred-interest medical financing arrangements charge substantial interest if the full balance is not cleared before the promotional period ends. Interest may then be calculated on the original financed amount rather than only on the remaining balance.

Patients should confirm:

- Whether the interest is genuinely zero or only deferred

- The date the promotional period ends

- The standard interest rate

- Whether one missed payment ends the promotion

- The minimum repayment

- The payment required to clear the balance on time

- Late fees

- Annual fees

- Whether the card can be used internationally

- Refund procedures after cancellation

Do not sign a financing agreement during a rushed consultation or immediately before surgery.

5. General-Purpose Credit Cards

A normal credit card may be accepted for deposits, flights, accommodation or treatment.

It can provide payment flexibility, but interest may become expensive when the balance is not cleared quickly.

Before paying, check:

- Purchase interest rate

- Foreign transaction fee

- Currency-conversion method

- Cash-advance charges

- Credit limit

- Payment due date

- Refund protection

- Dispute procedures

- Travel benefits

- Whether overseas medical treatment is excluded

Credit-card travel benefits should not automatically be treated as medical travel insurance. CDC guidance explains that card-related travel protections vary widely and should not replace appropriate travel health or medical evacuation insurance.

Avoid using multiple cards without a clear repayment schedule.

6. Borrowing from Family or Friends

Family support may offer greater flexibility than commercial credit, but unclear arrangements can damage relationships.

Create a written agreement covering:

- Amount borrowed

- Payment date

- Repayment schedule

- Interest, if any

- Missed-payment arrangements

- What happens if surgery is cancelled

- Whether early repayment is allowed

- Whether the money is a loan or gift

A complete budget should be prepared before borrowing. The borrower and lender should both understand how repayment may affect their household finances.

Patients should never assume that relatives will also pay for complications or extended stays.

7. Employer Benefits and Medical Savings Accounts

Some employers offer flexible benefits, health allowances or salary-linked savings schemes. Certain countries also provide tax-advantaged medical accounts.

Eligibility rules vary significantly. Purely appearance-related surgery may not qualify even when medically necessary procedures do.

For example, current United States tax guidance generally excludes procedures performed only to improve appearance from eligible medical expenses. Exceptions may apply when surgery corrects a deformity connected to a congenital condition, trauma or disfiguring disease.

Patients should consult the scheme administrator, accountant or qualified tax professional before assuming that:

- A cosmetic procedure is tax deductible

- An employer benefit will pay

- A medical savings account can be used

- Overseas treatment qualifies

- Travel and accommodation are eligible expenses

Tax and benefit rules depend on the country and individual circumstances.

8. Health Insurance for Medically Necessary Procedures

Elective cosmetic surgery is frequently excluded from standard health insurance. However, reconstructive or medically necessary procedures may sometimes qualify.

Examples may include surgery intended to address:

- Trauma-related deformity

- Congenital abnormality

- Functional breathing problems

- Reconstruction after cancer treatment

- Medically documented physical symptoms

Coverage depends on the policy, diagnosis, medical evidence, preauthorization requirements and treatment location.

Patients should ask their insurer:

- Is the procedure covered?

- Is preauthorization required?

- Must treatment be provided locally?

- Are overseas providers permitted?

- Are surgeon, hospital and anesthesia fees covered separately?

- Is complication care covered?

- Is revision treatment covered?

- Must the patient use an approved provider?

Obtain every coverage decision in writing.

9. Crowdfunding

Some patients raise funds through online crowdfunding platforms.

This method does not create normal loan repayments, but it involves:

- Public disclosure of personal information

- Platform and payment-processing fees

- Uncertain fundraising results

- Tax questions in some countries

- Pressure to proceed after receiving contributions

- Possible refund concerns when treatment is cancelled

Patients should protect their privacy and avoid publishing sensitive medical records, identity documents or financial details.

Receiving donations should not influence the surgeon’s assessment of whether treatment is appropriate.

10. Secured Borrowing

Secured loans use property, savings or another asset as security.

Although rates may appear lower, the consequences of non-payment can be serious. A patient may risk losing an important asset for an elective procedure.

Using a home, vehicle or essential family asset to finance cosmetic surgery should be approached with extreme caution and independent financial advice.

The lower monthly payment does not necessarily mean the borrowing is safer.

Financing Options Comparison Table

| Financing Method | Main Benefit | Main Risk | Important Question |

|---|---|---|---|

| Personal savings | No interest or debt | May reduce emergency savings | Will enough money remain for essential needs? |

| Provider payment plan | Payments may be divided | Terms may be unclear or linked to a lender | Is interest charged or deferred? |

| Personal loan | Fixed repayment structure may be available | Interest and long-term debt | What is the total repayment amount? |

| Medical credit card | Promotional financing may be offered | Deferred interest and high rates | What happens when the promotion ends? |

| General credit card | Convenient international payment | Interest and currency fees | Can the full balance be cleared quickly? |

| Family loan | Flexible terms may be possible | Relationship difficulties | Is there a written agreement? |

| Employer or medical account | May use available benefits | Cosmetic treatment may be excluded | Is the exact procedure eligible? |

| Insurance | May cover medically necessary care | Elective treatment often excluded | Is written preauthorization required? |

| Crowdfunding | No standard loan repayment | Privacy and uncertain funding | What fees and disclosure risks apply? |

| Secured loan | Potentially lower rate | Essential assets may be lost | Is the procedure worth placing the asset at risk? |

Building an International Cosmetic Surgery Budget

A structured budget should be created before selecting the final hospital.

Basic Budget Formula

Complete treatment budget =

Procedure quotation

- medical tests

- implants and supplies

- flights

- visa and travel documents

- accommodation

- local transportation

- meals

- companion expenses

- insurance

- medication

- follow-up care

- currency and payment fees

- income lost during recovery

- emergency reserve

This formula provides a more realistic picture than the procedure price alone.

International Treatment Budget Worksheet

| Budget Category | Hospital Estimate | Independent Estimate | Confirmed Amount |

|---|---|---|---|

| Surgeon’s fee | |||

| Hospital charges | |||

| Anesthesia | |||

| Medical tests | |||

| Implants or materials | |||

| Medication | |||

| Compression garments | |||

| Flights | |||

| Visa and documents | |||

| Accommodation | |||

| Companion expenses | |||

| Local transport | |||

| Food and daily needs | |||

| Travel health insurance | |||

| Medical evacuation cover | |||

| Follow-up at destination | |||

| Follow-up at home | |||

| Currency and bank fees | |||

| Lost earnings | |||

| Emergency reserve | |||

| Estimated total |

Patients should update this worksheet whenever the hospital, dates, destination or procedure changes.

Calculate the Cost of Time Away from Work

Recovery can affect income as well as medical spending.

Consider:

- Paid leave available

- Unpaid leave

- Self-employment income lost

- Reduced working hours

- Childcare

- Household assistance

- Support for dependants

- Additional leave if recovery is delayed

A patient who can afford the procedure but cannot manage several weeks of reduced income may not yet have a complete budget.

Do not base the return-to-work date only on a package advertisement. Recovery varies according to the procedure, work duties and individual healing.

Compare Plastic Surgery Costs by Country Carefully

Plastic surgery cost by country information can help identify general differences, but average prices do not represent individual quotations.

Costs may vary because of:

- Hospital type

- Surgeon experience

- City

- Procedure complexity

- Anesthesia method

- Length of surgery

- Implant choice

- Hospital stay

- Currency value

- International-patient services

- Aftercare included

BestCosmeticHospitals.com may help patients begin comparing areas such as:

- Rhinoplasty cost by country

- Liposuction cost by country

- Breast augmentation cost by country

- Tummy tuck cost by country

- Hair transplant cost by country

Every estimate should be confirmed directly with the hospital after a proper medical assessment.

Request an Itemized Hospital Quotation

Ask the hospital to separate each medical and non-medical charge.

The quotation should explain:

- Exact procedure

- Named surgeon

- Hospital location

- Anesthesia type

- Number of hospital nights

- Medical tests included

- Implant or product details

- Medication included

- Follow-up appointments

- Hotel and transfer arrangements

- Taxes

- Payment schedule

- Cancellation policy

- Revision policy

- Complication-related charges

- Quotation validity period

Do not accept phrases such as “all-inclusive” without a written definition of what is included and excluded.

Plan for Currency Changes and Payment Fees

International treatment is often priced in a different currency.

The final amount paid may change because of:

- Exchange-rate movement

- Card conversion rates

- Bank transfer fees

- Recipient-bank charges

- Foreign transaction fees

- Dynamic currency conversion

- Refund exchange-rate differences

Ask the hospital:

- Which currency is required?

- Is the price fixed in that currency?

- Which party pays transfer charges?

- When is the exchange rate determined?

- How are refunds calculated?

- Can payment be divided into a deposit and final balance?

- Will a receipt be issued for every payment?

Do not send money to a personal account without confirming why the payment is not being made to the licensed hospital or registered business.

Check Deposit, Cancellation and Refund Terms

Cosmetic surgery may be postponed because of:

- Unsuitable medical-test results

- Illness

- Pregnancy

- Visa refusal

- Flight cancellation

- Surgeon unavailability

- Hospital scheduling changes

- Patient decision

- Safety concerns identified during consultation

The written agreement should state:

- Deposit amount

- Refundable and non-refundable portions

- Cancellation deadline

- Administrative fees

- Rescheduling rules

- Refund processing time

- Currency used for refunds

- What happens when the provider cancels

- What happens when the surgeon changes

- Whether financing charges continue after cancellation

A non-refundable flight or hotel should not pressure a patient to continue with medically unsuitable treatment.

Budget for Insurance Separately

Travel disruption insurance, travel health insurance and medical evacuation insurance provide different types of protection. They may be sold separately or bundled, and one policy does not automatically replace another.

Patients should check whether a policy covers:

- Planned cosmetic treatment

- Complications from elective surgery

- Emergency hospital admission

- Additional accommodation

- Flight changes

- Medical evacuation

- Repatriation

- Pre-existing conditions

- A travelling companion

- Treatment after returning home

Some policies cover unrelated travel emergencies but exclude complications arising from planned procedures.

Request written confirmation rather than relying on a sales summary.

Create a Complication and Emergency Reserve

No responsible hospital can guarantee complication-free surgery.

The emergency budget may need to cover:

- Additional hospital nights

- Emergency tests

- Antibiotics

- Specialist consultations

- Wound treatment

- New flights

- Extended hotel accommodation

- Companion expenses

- Local emergency transportation

- Treatment after returning home

- Unpaid time away from work

CDC guidance advises medical travellers to understand the possible financial cost of emergency and follow-up care, which may need to be paid out of pocket.

The reserve should be accessible during travel and should not depend entirely on unused credit.

Test Whether the Financing Is Affordable

Before borrowing, calculate three figures:

Monthly Repayment

Can the payment be managed after rent, food, utilities, insurance, existing debts and family expenses?

Total Repayment

How much will the procedure cost after all interest and fees are added?

Financial Stress Test

Could repayments still be managed if:

- Income temporarily falls?

- Recovery takes longer?

- An emergency expense occurs?

- Interest increases on a variable-rate product?

- The procedure requires revision?

A monthly instalment may appear affordable while the total repayment remains excessive.

Postpone treatment when repayment would require borrowing for ordinary household expenses.

Questions to Ask a Finance Provider

Before signing, ask:

- What is the total amount borrowed?

- What is the annual interest rate or APR?

- Is the interest fixed, variable or deferred?

- What is the total repayment amount?

- How many payments are required?

- Are there processing or annual fees?

- What happens after a missed payment?

- Can the loan be repaid early?

- Is there an early-settlement charge?

- Does the lender pay the hospital directly?

- What happens when surgery is cancelled?

- How are refunds applied to the loan?

- Does the agreement affect the patient’s credit record?

- Is insurance included or added automatically?

- Which country’s laws govern the agreement?

Patients should receive enough time to review the agreement without pressure from a hospital representative.

Financial Warning Signs

Be cautious when a hospital, coordinator or lender:

- Focuses only on the monthly instalment

- Refuses to disclose the total repayment

- Calls deferred interest completely free

- Pressures the patient to sign immediately

- Adds insurance or fees without explanation

- Approves finance before medical assessment

- Encourages borrowing beyond the treatment cost

- Promises a refund without written terms

- Accepts payment only into a personal account

- Changes the quotation after the deposit

- Cannot explain complication costs

- Encourages secured borrowing for an elective procedure

- Suggests hiding the purpose of the loan

- Claims cosmetic surgery is automatically tax deductible

- Guarantees insurance reimbursement

Financing approval does not prove that treatment is affordable, appropriate or safe.

Common International Budgeting Mistakes

Patients should avoid:

- Comparing procedure prices without comparing inclusions

- Forgetting anesthesia and medical-test costs

- Ignoring companion expenses

- Booking the cheapest non-refundable flight

- Planning too few recovery nights

- Assuming ordinary travel insurance covers surgery

- Spending the entire budget on the procedure

- Having no emergency fund

- Depending on future credit approval

- Ignoring lost income

- Borrowing without reading cancellation terms

- Assuming revision treatment will be free

- Paying in an unfamiliar currency without checking fees

- Selecting a hospital mainly because finance is available

- Returning home early to reduce hotel costs

A complete budget should support safe treatment decisions rather than force the patient to compromise on recovery.

How BestCosmeticHospitals.com Supports Financial Research

BestCosmeticHospitals.com helps patients begin comparing:

- Best cosmetic hospitals in the world

- Best cosmetic surgeons in the world

- Cosmetic surgery abroad

- Best countries for plastic surgery

- Plastic surgery cost by country

- Procedure-specific cost factors

- Hospital services

- Treatment inclusions

- Recovery requirements

- International-patient support

The platform can help patients identify questions to ask and costs to compare before contacting providers.

It does not replace personal financial advice, medical assessment, insurance confirmation or independent verification of hospital and surgeon credentials.

Final Cosmetic Surgery Budget Checklist

Before booking treatment, confirm that you have:

- Received a complete medical assessment

- Verified the hospital and surgeon

- Obtained an itemized quotation

- Compared at least several suitable providers

- Calculated travel and accommodation costs

- Included companion expenses

- Estimated income lost during recovery

- Checked currency and payment fees

- Reviewed insurance exclusions

- Planned local follow-up care

- Created an emergency reserve

- Compared the total cost of every financing option

- Read deposit and refund terms

- Understood the revision policy

- Confirmed complication-related charges

- Tested monthly repayment affordability

- Avoided using essential household funds

- Kept copies of contracts and receipts

- Prepared to delay surgery when the budget is incomplete

Frequently Asked Questions

1. Can cosmetic surgery be paid for in monthly instalments?

Some hospitals and finance companies offer instalment plans. Patients should check whether interest, processing fees or deferred-interest conditions apply and compare the total repayment.

2. Is a medical credit card interest-free?

Not always. Some products offer temporary promotional periods. Interest may become payable when the balance is not fully cleared within the required time.

3. Is a personal loan suitable for cosmetic surgery?

A personal loan may offer scheduled repayments, but it increases the procedure’s total cost. The patient should assess repayment affordability and compare alternatives carefully.

4. Does health insurance cover cosmetic surgery abroad?

Purely elective procedures are often excluded. Reconstructive or medically necessary treatment may sometimes qualify, depending on the policy and preauthorization requirements.

5. What costs are usually missing from advertised surgery packages?

Advertisements may exclude anesthesia, tests, implants, medication, additional hospital nights, flights, accommodation, follow-up care and complication treatment.

6. How much emergency money should a patient keep?

There is no universal amount. The reserve should reflect the procedure, destination, insurance exclusions, possible flight changes and estimated emergency medical costs.

7. Should patients borrow from family for cosmetic surgery?

Family borrowing may be flexible, but the terms should be documented clearly. Both sides should understand repayment, cancellation and relationship risks.

8. Are international cosmetic surgery costs tax deductible?

Tax treatment varies by country. Purely appearance-related procedures may not qualify, while certain reconstructive treatments may receive different treatment under local rules.

9. What happens to financing when surgery is cancelled?

The answer depends on the lender and hospital agreements. Patients should confirm whether the payment is refunded directly to the lender and whether fees or interest remain payable.

10. Is choosing the lowest-cost country a good budgeting strategy?

Not by itself. Hospital quality, surgeon qualifications, travel costs, aftercare and complication planning may make a slightly higher treatment price financially safer overall.

Conclusion

Cosmetic surgery financing should be evaluated with the same care as the surgeon, hospital and destination.

Personal savings may offer the lowest financial risk, while payment plans, personal loans and credit products can make treatment accessible sooner. However, borrowing adds interest, fees and repayment responsibilities that continue regardless of the surgical outcome.

International patients should budget for more than the operation. Flights, accommodation, medical tests, medication, aftercare, insurance, lost income and possible complications all affect the true cost.

BestCosmeticHospitals.com can provide a structured starting point for comparing hospitals, specialists, destinations, procedures and estimated prices. Patients should make the final decision only after reviewing their medical suitability, complete financial position and ability to manage unexpected costs.